Does Each Individual Need Renters Insurance?

You just signed a lease with two of your closest friends. The landlord hands over the keys, and someone in the group asks

“Do we all need renters insurance, or can we just share one policy?”

It’s a fair question. And honestly, most people don’t know the answer until something goes wrong. A laptop gets stolen. A fire breaks out. Someone slips and falls in your apartment. Suddenly, who has coverage and who doesn’t becomes a very real, very expensive problem.

The short answer is yes — in most cases, each individual

does need their own renters insurance. But the full picture is a bit more nuanced than that. Whether you’re living alone, splitting rent with a roommate, or packing into a three-bedroom with multiple tenants, this guide will walk you through everything you need to know about renters insurance and how it actually works when multiple people share a space.

What Is Renters Insurance, and Why Does It Matter?

Before we get into the roommate specifics, let’s make sure we’re on the same page about what renters insurance actually covers.

Renters insurance is a type of insurance policy designed for people who rent their home rather than own it. Your landlord’s insurance covers the building itself — the walls, the roof, the plumbing. But it does

not cover your personal belongings or protect you from liability. That’s where renters insurance comes in.

A standard renters insurance policy typically includes three core protections:

- Personal Property Coverage: Pays to repair or replace your belongings if they’re stolen, damaged by fire, vandalism, or certain other covered events.

- Liability Protection: Covers you if someone is injured in your home or if you accidentally cause damage to someone else’s property.

- Additional Living Expenses (ALE): Helps pay for temporary housing and extra costs if your rental becomes uninhabitable due to a covered loss.

According to the Insurance Information Institute (III), the average renters insurance policy costs around $15 to $30 per month — a relatively small price for meaningful financial protection.

Now, here’s where roommates come in and Does Each Individual Need Renters Insurance?

Is Renters Insurance Per Person or Per Unit?

This is one of the most commonly searched questions when it comes to renters insurance, and it’s easy to see why. The confusion usually comes from the way most policies are structured.

Renters insurance is issued per policyholder, not per unit. That means a policy only covers the person named on it — and in some cases, a named additional insured — not every person living in the apartment automatically.

If you live alone, this is simple: you get one policy, you’re covered. But if you share an apartment with one or more roommates, each person’s belongings and liability exposure are technically separate. One roommate’s policy generally does

not extend coverage to another roommate’s things unless they are specifically listed on that policy and make sure for Does Each Individual Need Renters Insurance?.

Does Each Roommate Need Their Own Renters Insurance?

In most situations, yes — each roommate should have their own separate renters insurance policy. Here’s why that matters in practice.

Your Stuff Is Not Their Stuff

Let’s say your roommate has renters insurance but you don’t. Someone breaks into your apartment and steals your laptop, your gaming console, and your camera equipment. Your roommate’s policy will reimburse their stuff. Not yours. You’re left paying out of pocket.

Liability Is Personal

Liability claims are tied to the individual. If a guest trips and gets injured in the living room, whose liability policy applies? The one belonging to the person they were visiting, or the policyholder? Without your own policy, you could be personally on the hook for medical bills or legal costs.

Some Landlords Require It Per Tenant

Many landlords and property management companies now require every adult tenant on the lease to carry their own renters insurance policy. Always read your lease carefully. If the lease says each tenant must have coverage, sharing one policy between roommates won’t satisfy that requirement.

Can Roommates Share One Renters Insurance Policy?

Technically, yes — some insurance companies do allow you to add a roommate to your policy as an additional insured. But this approach comes with some important limitations that most people don’t fully understand before they agree to it.

How Adding a Roommate to Your Policy Works

When you add someone as an additional insured or additional named insured to your renters policy, they gain access to some of the coverage. However, this usually means:

- The policy’s total coverage limits are shared between both of you — not doubled.

- Claims filed by either person affect the same policy and can raise premiums for both.

- If you have a falling out with your roommate and one of you moves out, separating the policy can get complicated.

- Not all insurers allow roommate additions on personal renters policies.

The Smarter Alternative: Separate Policies

Most insurance professionals recommend that each roommate get their own individual policy. Here’s why it actually makes more sense financially and practically:

- Each person has their own coverage limits, so a claim by one roommate doesn’t reduce what’s available to the other.

- Your insurance history and premium stay separate from your roommate’s.

- When someone moves out, there’s nothing to untangle or divide.

- Each person can customize their coverage based on the value of their own belongings.

Given that renters insurance is genuinely affordable — often less than a couple of streaming subscriptions per month — there’s really no strong financial argument for sharing. It’s just not worth the risk.

Does Renters Insurance Cover All Tenants in an Apartment?

Not automatically. A renters insurance policy issued in your name covers you. In most states and with most insurers, coverage also extends to:

- Your spouse or domestic partner

- Your dependent children living with you

- Other relatives living in your household (varies by insurer)

But a random roommate who is not related to you and not listed on your policy? They are

not covered. Their belongings, their liability — none of it falls under your policy by default.

This is a common and costly misunderstanding. If you and your roommate both assume one of you has everyone covered, you could end up in a situation where neither of you is truly protected.

Does Each Individual Need Renters Insurance

Renters Insurance With Multiple Roommates: How It Works

If you’re living with two or three roommates — say in a three-bedroom apartment — the same principles apply, just multiplied. Let’s walk through a realistic scenario.

Scenario: Three Roommates, One Apartment

Roommate A has renters insurance. Roommates B and C do not.

A pipe bursts in the kitchen, causing water damage and ruining electronics and furniture belonging to all three roommates. The building’s plumbing is covered by the landlord’s insurance. But the personal property inside?

- Roommate A: Files a claim, gets reimbursed for their damaged belongings.

- Roommate B: No coverage. Replaces everything out of pocket.

- Roommate C: Same situation as B. No coverage, full financial hit.

For renters insurance with 3 roommates, the ideal setup is straightforward: every single person gets their own individual policy. Each person pays their own modest premium, maintains their own coverage limits, and protects their own stuff independently.

It avoids disputes, simplifies claims, and gives everyone peace of mind without any complicated arrangements.

Can You Have Two Renters Insurance Policies at Once?

This is a question that comes up more often than you’d think, especially for people who are in between living situations or who have two residences. The short answer is: technically yes, but there are important caveats.

Having two renters insurance policies at the same time is generally allowed, but insurance is meant to

indemnify you — meaning it covers your actual loss, not double it. If you file a claim with both insurers for the same loss, the companies will coordinate to avoid paying out more than the total value of your loss. This is called the coordination of benefits principle.

In practical terms, having two renters insurance policies is rarely advantageous. You’d be paying two premiums but not necessarily receiving double the protection on any single claim. The better approach is to have one comprehensive policy with coverage limits appropriate for the total value of your belongings.

There are edge cases where carrying two policies makes sense — such as when you’re moving and briefly maintaining two residences simultaneously. But as a long-term strategy, it’s generally not recommended.

How to Add a Person to Renters Insurance

If you’ve decided that adding someone to your renters policy is the right move — perhaps for a significant other or a family member — here’s what the process generally looks like.

- Contact your insurer: Call or log into your account and request to add an additional insured or additional named insured to your policy.

- Provide their information: Name, date of birth, and sometimes their relationship to you.

- Review the updated coverage: Make sure the policy limits are sufficient for both people’s belongings combined.

- Confirm any premium changes: Adding another person may or may not affect your monthly rate.

- Get it in writing: Always request a new declarations page confirming both names are on the policy.

Keep in mind that not every insurer allows roommates (as opposed to domestic partners or family members) to be added. If your insurer doesn’t offer this option, the answer is simple: each of you gets your own policy.

Does Every Renter Need Renters Insurance? What State Law Says

No state currently requires renters to carry renters insurance by law. However, landlords are legally permitted to require it as a condition of your lease — and many do.

Landlord requirements vary by state and even by city. In competitive rental markets, it’s increasingly common to see renters insurance listed as a mandatory lease requirement for every adult tenant named on the lease.

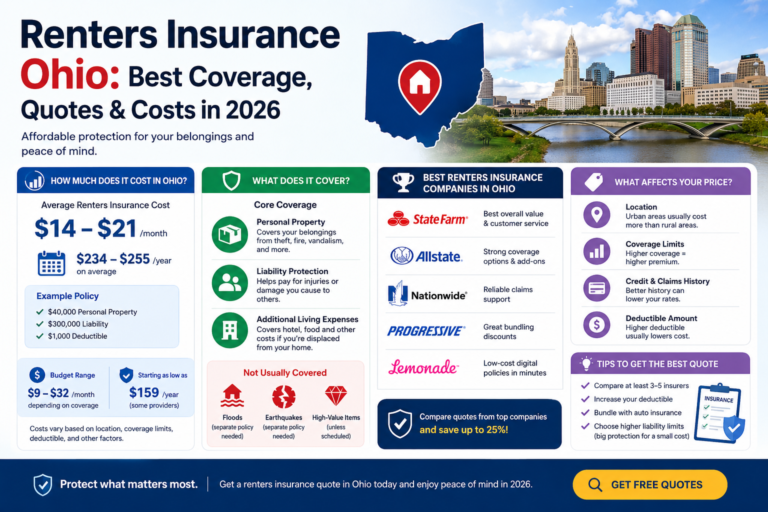

If you’re renting in Ohio, for example, landlords in cities like Columbus, Cleveland, and Cincinnati have been increasingly adding renters insurance clauses to their standard leases. If you’re navigating this in the Buckeye State, our detailed guide on renters insurance in Ohio covers everything from coverage requirements to the best local providers.

Regardless of whether your landlord requires it, having renters insurance is simply good financial sense. The National Association of Insurance Commissioners (NAIC) consistently recommends renters insurance as one of the most cost-effective forms of consumer protection available.

Roommate Insurance: What Policies Actually Cover Roommates?

Some insurers market specific products sometimes loosely called “roommate insurance” — these are essentially standard renters policies that explicitly allow an additional roommate to be named on the policy. They’re not a fundamentally different product, just a variation in how the policy is structured.

When evaluating renters insurance that includes roommates, look for the following features:

- Clear definition of who is covered: Both names should appear on the declarations page.

- Separate or shared coverage limits: Understand whether the limit is pooled or individual.

- Liability coverage for each person: Confirm both roommates have liability protection, not just one.

- Policy flexibility: What happens if one roommate moves out mid-term?

The III recommends reading your policy declarations page carefully and calling your insurer directly if you have any questions about who is and isn’t covered under your plan.

How to Share Renters Insurance With Roommates: Step-by-Step

If after reviewing your options, you’ve decided you want to share a renters insurance policy with a roommate, here’s a practical step-by-step approach to do it the right way.

- Inventory your belongings: Both roommates should create a home inventory listing all valuables — electronics, furniture, clothing, jewelry, instruments, etc. — and their estimated replacement value.

- Choose adequate limits: Add up the total replacement value for both roommates’ belongings and make sure your coverage limit reflects that combined amount.

- Confirm eligibility with your insurer: Not all insurers allow non-related roommates to be added. Verify this before assuming it’s possible.

- Get both names on the declarations page: This is non-negotiable. Verbal agreements don’t count when it comes to insurance.

- Agree on claims procedures: Before anything happens, agree on who handles communications with the insurer and how any payout is divided.

- Review when someone moves: Set a reminder to update or separate the policy if living arrangements change.

Again, most insurance professionals still recommend separate policies. But if sharing is your chosen path, following these steps at least ensures you’re doing it correctly.

Why So Many Renters Skip Insurance (And Why That’s a Mistake)

According to data from the U.S. Census Bureau, roughly 36% of Americans rent their homes. Yet surveys consistently show that a significant portion of renters don’t have renters insurance — despite it being one of the most affordable types of coverage available.

The most common reasons people skip renters insurance:

- “I don’t own that much stuff.” Most people dramatically underestimate the total value of their belongings. Add up your laptop, TV, phone, clothes, kitchen appliances, and furniture — it adds up fast.

- “My landlord’s insurance covers me.” It doesn’t. Your landlord’s policy covers the building structure, not your personal property.

- “I’ll get it later.” Disasters don’t send calendar invites. Theft, fire, and water damage can happen any time.

- “My roommate has it.” As we’ve covered at length: your roommate’s policy almost certainly does not cover your belongings.

The financial risk of going without renters insurance simply isn’t worth it, especially when coverage is this accessible and affordable. The Consumer Financial Protection Bureau (CFPB) notes that unexpected financial shocks — exactly the kind an uninsured renter faces after a theft or fire — are a leading contributor to financial instability.

What to Look for in a Renters Insurance Policy as a Renter With Roommates

When shopping for your own renters insurance policy — or evaluating whether to add a roommate — here are the key policy features to pay attention to.

Coverage Limits

This is the maximum amount the insurer will pay out on a claim. Make sure your limits reflect the actual replacement value of your belongings. Most policies default to $15,000–$30,000 in personal property coverage, but you can often adjust this.

Actual Cash Value vs. Replacement Cost

Actual cash value (ACV) pays what your item is worth today (accounting for depreciation). Replacement cost value (RCV) pays what it actually costs to replace the item new today. RCV coverage is generally the better choice, even if it costs slightly more.

Liability Coverage Amount

Most policies include $100,000 in liability coverage as a baseline. Depending on your situation, you may want to consider higher limits — especially if you regularly host people at your apartment.

Deductible

This is what you pay out of pocket before insurance kicks in. A higher deductible means a lower premium but more out of pocket at claim time. Find a balance that makes sense for your financial situation.

Insurer Reputation and Financial Strength

Always check your insurer’s financial stability rating through AM Best and customer satisfaction scores through J.D. Power. A cheap policy from an insurer who won’t pay claims promptly isn’t a bargain.

Frequently Asked Questions

Final Thoughts

Living with roommates is a practical, often necessary part of renting in today’s housing market. But shared living arrangements don’t mean shared insurance coverage — at least not automatically.

The bottom line is this: each individual renter benefits from having their own renters insurance policy. It’s not expensive, it’s not complicated, and the protection it provides is real. Whether you have a single roommate or you’re sharing a place with three or four people, getting your own coverage is the smartest, simplest move you can make.

Don’t assume your roommate’s policy has you covered. Don’t assume your landlord’s insurance protects your stuff. Take 15 minutes, get a quote, and get covered.