Everything Renters Need to Know

Does Renters Insurance Cover Earthquakes: Let’s be honest — most people don’t think about earthquakes until the ground actually starts shaking. And by then, it’s too late to wonder whether your renters insurance has you covered.

If you’re renting an apartment, a house, or a condo, you might already have a renters insurance policy in place. Good for you — most renters don’t. But here’s the thing a lot of people don’t find out until after disaster strikes: standard renters insurance does not cover earthquake damage.

That’s not a typo. Your policy won’t pay for your damaged furniture, broken electronics, cracked walls, or the hotel bill you rack up while your rental is being repaired — not if an earthquake caused it.

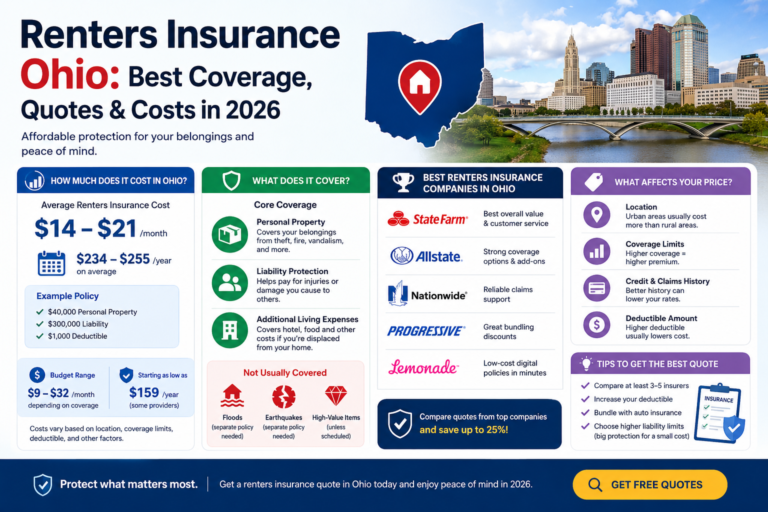

This guide breaks down exactly what renters insurance covers, why earthquakes are excluded, and what you can actually do to protect yourself. Whether you’re renting in California, Ohio, or anywhere else in the U.S., this is information worth knowing before the ground moves.If you’re an Ohio renter specifically, we’ve put together a complete renters insurance Ohio coverage guide that covers everything from average costs to the best providers in the state.

What Does a Standard Renters Insurance Policy Actually Cover?

Before we get into the earthquake exclusion, it helps to understand what renters insurance is designed to do in the first place.

A basic renters insurance policy typically covers three main things:

- Personal Property: This is the big one. If your laptop, couch, TV, clothes, or kitchen appliances are stolen or damaged in a covered event, your insurance pays to repair or replace them.

- Liability Protection: If someone gets hurt in your rental or you accidentally damage someone else’s property, your policy covers the legal and medical costs up to your policy limit.

- Additional Living Expenses (ALE): If your rental becomes uninhabitable due to a covered event — a fire, for example — your policy pays for your hotel stay, meals, and other temporary living costs.

Covered events typically include fire, smoke, theft, vandalism, windstorms, hail, and certain types of water damage (like a burst pipe, not a flood). These are called named perils, and your policy will list them explicitly.

For a broader look at what renters insurance covers — including renters insurance liability and personal property coverage — it’s worth reviewing your policy in detail or speaking with your insurer.

Now here’s where most renters get surprised: earthquakes are not on that list.

Does Renters Insurance Cover Earthquakes? The Short Answer

No. Standard renters insurance does not cover earthquake damage.

This isn’t a gray area or something that varies from policy to policy. It’s a universal exclusion across nearly every major insurance provider in the United States. Whether you have coverage through GEICO, State Farm, Lemonade, Allstate, or a smaller regional insurer — earthquake damage is excluded from your standard renters policy.

The Insurance Information Institute (III) confirms this clearly: homeowners and renters insurance does not cover earthquake damage. Period.

What does that mean in practical terms? If a 6.0 magnitude earthquake hits your city tonight and cracks your walls, knocks your TV off the stand, shatters your dishes, and forces you to stay in a hotel for three weeks — your standard renters policy won’t pay for any of it.

That’s a significant financial gap. And it’s one that most renters don’t discover until it’s too late.

Why Are Earthquakes Excluded From Renters Insurance?

It’s a fair question. Why would insurance companies exclude something as unpredictable and damaging as an earthquake?

The answer comes down to risk.

Insurance works because not everyone files a claim at the same time. When your neighbor’s apartment floods, yours probably doesn’t. When someone’s car gets stolen, it’s an individual event. Insurers can spread that risk across thousands of policyholders and keep premiums affordable.

Earthquakes don’t work that way. When a major earthquake hits, it damages hundreds or thousands of properties simultaneously in the same area. Insurers would face a massive wave of claims all at once — far more than their standard premium pool could absorb.

Because of this, earthquake coverage requires its own pricing model, its own risk assessment, and its own policy structure. It simply doesn’t fit inside the framework of standard renters insurance.

That’s why earthquake coverage is always sold separately — either as a standalone policy or as an add-on endorsement to your existing renters policy.

What About Other Natural Disasters? Does Renters Insurance Cover Earthquakes Those?

This is where things get a little more nuanced.

Renters insurance covers some natural disasters but not others. Here’s a quick breakdown:

Covered by Standard Renters Insurance:

- Lightning strikes: If lightning hits your building and damages your belongings, that’s typically covered.

- Windstorms and hail: Damage from strong winds or hailstorms is usually included.

- Fire (including wildfires in some cases): Fire damage to your personal property is a standard covered peril.

- Smoke damage: Often covered alongside fire damage.

- Burst pipes and sudden water damage: Accidental discharge or overflow from plumbing is typically covered.

NOT Covered by Standard Renters Insurance:

- Earthquakes: Excluded universally. Requires separate coverage.

- Floods: Also excluded. Flood damage requires a separate flood insurance policy, typically through the National Flood Insurance Program (NFIP).

- Sinkholes: Generally excluded, though some states require limited sinkhole coverage.

- Landslides and mudslides: Excluded from standard policies.

- Tsunami damage: Also excluded, as it falls under flood/earth movement exclusions.

The pattern here is clear: anything classified as “earth movement” or “flooding” is excluded from standard renters insurance. These events require specialized coverage.

What Does Earthquake Damage Actually Cost Renters?

Let’s put some real numbers to this so the stakes are clear.

The average renter owns somewhere between $20,000 and $30,000 worth of personal belongings. That includes furniture, electronics, clothing, kitchen equipment, bicycles, and everything else that makes a rental feel like home.

After a moderate to major earthquake, here’s what you might be looking at:

- Furniture replacement: $3,000 – $8,000 for a full apartment’s worth of furniture

- Electronics: $2,000 – $5,000 for TV, laptop, gaming systems, appliances

- Temporary housing: $1,500 – $4,000/month for a hotel or short-term rental

- Food and transportation: $500 – $1,500 per month in additional costs

- Emergency repairs: $500 – $2,000 for immediate fixes to prevent further damage

A significant earthquake could easily cost a renter $15,000 to $30,000 or more out of pocket — with zero help from their standard renters policy.

For many renters, that’s financially devastating.

How to Get Earthquake Coverage as a Renter

The good news: you’re not stuck. There are two main ways to get earthquake coverage as a renter.

Add an Earthquake Endorsement to Your Renters Policy

Many insurance companies allow you to add earthquake coverage as an endorsement — also called a rider — to your existing renters insurance policy. This is often the simplest and most affordable option.

With an endorsement, you don’t need to manage a separate policy. Your earthquake coverage sits alongside your standard renters policy and activates when an earthquake causes damage to your belongings or forces you out of your rental.

Providers like GEICO offer earthquake insurance options that can be layered onto renters coverage, particularly in high-risk states like California, Oregon, and Washington.

Buy a Standalone Earthquake Insurance Policy

In some cases — especially in California — you may need or prefer a standalone earthquake insurance policy.

In California, most earthquake insurance for renters is available through the California Earthquake Authority (CEA), a not-for-profit organization backed by the state government. The CEA works with over 20 participating insurance companies to offer affordable earthquake coverage to renters, homeowners, and condo owners.

A CEA renters policy typically covers:

- Personal property damage up to your chosen limit

- Loss of use / additional living expenses — with no deductible

- Emergency repairs — first $1,500 with no deductible

You must have an existing renters insurance policy with a CEA-participating insurer to add CEA earthquake coverage. Your insurer can set this up for you — you don’t need to wait until your policy renews.Outside California, State Farm and Liberty Mutual also offer earthquake endorsements for renters in many states.

How Much Does Earthquake Insurance Cost for Renters?

Cost is usually the first question renters ask — and the answer is more encouraging than most people expect.

Because renters are only covering their personal belongings (not the building itself), earthquake insurance for renters is significantly more affordable than earthquake coverage for homeowners.

Here’s a general ballpark:

- Low-risk states: $30 – $100 per year

- Moderate-risk states: $100 – $300 per year

- High-risk states (California, Oregon, Washington): $150 – $800+ per year, depending on location, building type, and coverage limits

Deductibles for earthquake insurance are typically higher than standard renters insurance deductibles — often 5% to 25% of your coverage limit. So if you have $20,000 in personal property coverage with a 10% deductible, you’d pay the first $2,000 out of pocket before coverage kicks in.

That said, a $200/year premium and a $2,000 deductible beats a $20,000 out-of-pocket bill by a long shot.

The CEA offers an online premium calculator on their website so California renters can get an accurate estimate for their specific location and coverage needs.

What Does Earthquake Insurance for Renters Cover?

A standard earthquake insurance policy for renters typically covers the following:

Personal Property

This is the core coverage. If your furniture, electronics, clothing, appliances, and other belongings are damaged or destroyed by an earthquake, your policy pays to repair or replace them up to your chosen coverage limit.

Some policies cover replacement cost value (what it costs to buy new), while others cover actual cash value (what your items are worth after depreciation). Replacement cost coverage is always better — make sure you know which one your policy offers.

Loss of Use / Additional Living Expenses

If your rental is so damaged that you can’t live there, earthquake insurance covers your temporary living costs — hotel bills, short-term rental costs, increased food expenses, and other costs above your normal monthly budget.

The CEA’s loss of use coverage has no deductible, which is a significant benefit. The coverage limit varies based on the plan you choose.

Emergency Repairs

Immediate repairs needed to keep your rental safe after an earthquake — boarding up broken windows, removing dangerous debris, tarping openings to prevent rain damage — are typically covered up to a set limit.

What Earthquake Insurance Does NOT Cover

- Damage to the building itself (that’s your landlord’s responsibility)

- Vehicles (covered under comprehensive auto insurance)

- Pre-existing damage

- Flood damage that follows an earthquake (requires separate flood insurance)

- Business property or equipment used for work

Do You Really Need Earthquake Insurance? Here’s How to Decide

Not every renter needs earthquake insurance. But far more renters need it than currently have it.

Here are the key factors to consider:

Where Do You Live?

The most important factor is your location. The U.S. Geological Survey tracks seismic activity across the country, and the risk is not limited to California.

High-risk states include California, Oregon, Washington, Alaska, and Hawaii. But significant earthquake risk also exists in:

- Oklahoma (due to increased seismic activity from oil drilling)

- The New Madrid Seismic Zone (Missouri, Arkansas, Tennessee, Kentucky, Illinois)

- South Carolina

- Nevada

- Montana and Idaho

Ohio — where the New Madrid fault zone creates some risk — is worth considering for renters who want to be thorough. If you want a complete picture of coverage options for Ohio renters, our renters insurance Ohio coverage guide walks through the specifics in detail.

How Much Could You Afford to Lose?

Think about what it would cost to replace everything you own. Now imagine doing that with zero insurance help. If that scenario would cause serious financial hardship — and for most renters it would — earthquake insurance is worth the relatively small annual premium.

What Type of Building Do You Live In?

Older wood-frame buildings, soft-story apartment buildings, and buildings on soft soil or near fault lines face higher earthquake risk. Newer buildings built to modern seismic codes are more resilient, but no building is immune.

Does Your Landlord’s Policy Cover You?

It doesn’t. Your landlord’s insurance covers the building structure. It does not cover your personal belongings, your liability, or your temporary living expenses. You are entirely responsible for your own possessions.This is also true for other types of coverage — if you’ve ever wondered whether every renter needs their own policy, the answer is almost always yes.

What Happens If You Don’t Have Earthquake Insurance?

If an earthquake damages your rental and you don’t have earthquake coverage, your options are limited — and none of them are great.

FEMA Assistance

After a federally declared disaster, FEMA may provide some financial assistance. But FEMA aid is not guaranteed, takes time to process, and is often far less than the actual losses. FEMA reports that its average individual assistance payout is around $5,000 — a fraction of what most renters lose in a major earthquake.

FEMA assistance is also only available after a presidential disaster declaration, which doesn’t happen after every earthquake. Smaller quakes — which can still cause significant personal property damage — typically don’t qualify.

SBA Disaster Loans

The Small Business Administration (SBA) offers low-interest disaster loans to renters and homeowners in declared disaster areas. These can help, but they’re loans — not grants. You’ll need to repay them.

Out of Pocket

For most renters, the reality is that uninsured earthquake losses come out of their own savings — or go on credit cards. That’s a financial setback that can take years to recover from.

The math is straightforward: a $150 annual premium is an easy trade-off compared to a $15,000 unexpected expense.

Earthquake Insurance vs. Renters Insurance

Let’s put this side by side so it’s crystal clear:

- Standard Renters Insurance covers: fire, theft, vandalism, windstorm, burst pipes, liability, additional living expenses (for covered events)

- Earthquake Insurance covers: earthquake damage to personal property, loss of use after an earthquake, emergency repairs

- Neither covers: floods, sinkholes, landslides, tsunamis (all require separate policies)

Your landlord’s insurance covers: the building structure only — not your belongings or your living expenses

These are separate, complementary policies. For renters in earthquake-prone areas, carrying both standard renters insurance and earthquake coverage gives you the most complete protection.For a deeper look at earthquake insurance options across providers, the Insurance Information Institute is an excellent resource. United Policyholders also offers a detailed earthquake insurance guide for renters that’s worth reading.

Frequently Asked Questions

Final Thoughts: Don’t Wait Until the Ground Shakes

Here’s the bottom line: renters insurance is important, but it doesn’t cover everything. Earthquakes are one of the most significant gaps in standard coverage — and one of the most expensive gaps to discover the hard way.

If you live in an earthquake-prone area, adding earthquake coverage is one of the most cost-effective financial decisions you can make as a renter. The annual premium is manageable. The potential loss without coverage is not.

Start by reviewing your current renters insurance policy to understand what’s covered. Then contact your insurer and ask about earthquake endorsements or standalone policies available in your state.

And if you’re an Ohio renter looking to understand your full coverage options — from standard renters insurance to natural disaster protection — our renters insurance Ohio coverage guide is the best place to start.