What Every Dog Owner Needs to Know

Let me be straight with you — most renters with dogs have no idea what their policy actually covers. They sign up, pay the monthly premium, and assume they are protected. Then something happens. Their dog bites a neighbor. A guest trips over the dog and breaks a wrist. Suddenly they are staring at a $40,000 medical bill with zero coverage.

That situation is more common than people realize. And it is entirely avoidable.

This guide is specifically about renters insurance with dog bite coverage — what it actually includes, where the gaps are, which dog breeds cause problems, and how to find pet renters insurance that genuinely protects you. Whether your dog is a laid-back lab or a breed that insurance companies love to restrict, there is a path to proper coverage. You just need to know where to look.

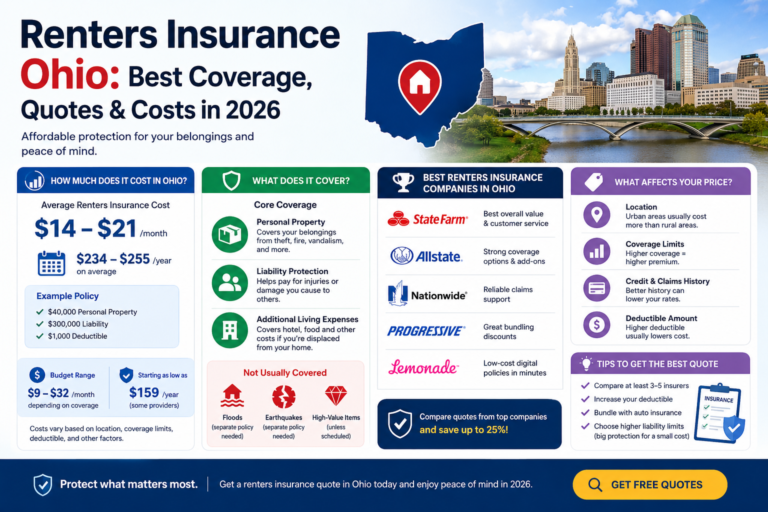

If you are an Ohio renter, our detailed breakdown of renters insurance in Ohio is a great starting point before diving into pet-specific coverage.

So Does Renters Insurance Actually Cover Dogs?

Yes — most of the time. But the word “most” is doing a lot of heavy lifting in that sentence.

Standard renters insurance includes personal liability coverage. That liability coverage is what kicks in when your dog injures someone. If your dog bites a visitor in your apartment, your policy can pay for their medical treatment, their legal fees if they sue, and any settlement or judgment against you — all up to your policy’s liability limit.

So when people ask does renters insurance cover dogs, the technically accurate answer is: it covers the liability your dog creates, not the dog itself.

Here is where people get confused though. There are two completely different types of protection people think about:

- Liability coverage: Pays when your dog hurts someone else. This is what most renters policies include.

- Property damage coverage: Pays when your dog damages stuff. Almost no standard renters policy covers this for pet-caused damage — including damage to your own belongings.

So if your dog bites your neighbor? Covered. If your dog chews through your leather sofa? That is your problem.

The Insurance Information Institute reports that dog bites and related injuries make up more than one-third of all homeowners and renters liability claims by dollar value — with the average payout now exceeding $64,000 per incident. That number alone should tell you why renters insurance with dog bite coverage deserves serious attention.

What Is Covered and What Is Not — The Honest Breakdown

People shopping for renters insurance with pet coverage often discover coverage gaps the hard way. Here is a clear picture of what you should expect from a standard policy.

Things Your Policy Typically Covers

- A guest bitten by your dog inside or outside your apartment

- Medical bills for the injured party, even if no lawsuit is filed

- Attorney fees and court costs if someone takes you to court

- Settlements and judgments — up to your liability limit

- Injuries beyond bites — like your dog knocking an elderly neighbor down the stairs

Things That Are Almost Never Covered

- Renters insurance cover pet damage to your own property — furniture, floors, clothing — is excluded in virtually every standard policy

- Damage your dog causes to the rental unit — that comes out of your security deposit

- Injuries to you or other household members

- Incidents involving a breed your insurer has restricted or excluded

- Any incident involving a dog you failed to disclose to your insurer

- Bite incidents involving a dog with a documented prior bite history — many carriers will not touch this

The question does renters insurance cover pet damage trips people up constantly. The short answer: not to your own stuff, and not to your rental unit. What pet renters insurance actually protects is your financial exposure to third parties — the people your dog might injure.

Worth knowing: Some landlords now require proof of pet liability insurance for renters before allowing a dog in the unit. Even if yours does not, having it is smart protection.

The Real Cost of a Dog Bite — And Why Coverage Matters

People underestimate how expensive a dog bite incident can get. A small bite that barely breaks the skin can still lead to a lawsuit. A serious bite — one involving a child’s face, for example — can spiral into costs that would wipe out most people’s savings entirely.

Here is a realistic look at what dog liability insurance for renters might need to cover if your dog is involved in a serious incident:

| What You Could Owe | Realistic Cost Range |

| Emergency room treatment | $800 – $6,000 |

| Reconstructive or plastic surgery | $15,000 – $60,000+ |

| Lost wages for the victim | $3,000 – $25,000+ |

| Pain and suffering damages | $20,000 – $150,000+ |

| Your own legal defense | $8,000 – $35,000+ |

| Total exposure (serious incident) | $50,000 – $275,000+ |

These numbers are not extreme outliers. They reflect real claims that happen every year across the country. The American Veterinary Medical Association estimates roughly 4.5 million dog bites occur annually in the US, with around 800,000 requiring medical attention. A meaningful percentage of those lead to legal action.

Without renters insurance with dog bite coverage, you are personally on the hook for every dollar. Your savings, your paycheck, potentially your future earnings. Canine liability coverage is not about being paranoid — it is about being realistic about what dog ownership actually involves.

State law adds another layer of complexity. Some states hold dog owners strictly liable for any bite, regardless of whether the dog had any history of aggression. Others follow a one-bite rule. Understanding where your state falls matters when assessing your risk. Nolo’s dog law resources are a good starting point for that research.

Breed Restrictions: The Conversation Nobody Wants to Have

Here is the uncomfortable truth about renters insurance that covers dogs: not all dogs are treated equally. Insurance companies maintain lists of breeds they consider high-risk, and if your dog is on that list, you may find yourself declined, excluded, or paying significantly more.

This hits hardest for people looking for renters insurance with pitbull coverage. Pit bulls, along with a handful of other breeds, appear on the restricted list of almost every major insurer. That does not mean coverage is impossible — it means you have to shop differently.

Breeds That Frequently Face Restrictions

- Pit Bulls and American Staffordshire Terriers

- Rottweilers

- Doberman Pinschers

- German Shepherds

- Chow Chows

- Akitas

- Siberian Huskies and Alaskan Malamutes

- Wolf-dog hybrids and mixed breeds with suspected restricted lineage

If your dog falls into one of these categories, your approach to finding renters insurance with dog bite coverage needs to change. Standard carriers like State Farm or Allstate may decline entirely. But specialty insurers and surplus lines companies — the ones that underwrite risks mainstream companies avoid — often have options.

One important point: never lie about your dog’s breed on an insurance application. If your dog bites someone and the insurer discovers you misrepresented the breed, they can deny the claim and cancel your policy. The short-term convenience of hiding the breed is not worth the catastrophic downside.

Good news: Some states have passed laws that prohibit insurance companies from denying or canceling coverage based solely on dog breed. Check your state’s laws before assuming you have no options with your current insurer.

For those with restricted breeds, dog owner liability insurance through a standalone policy is usually the most practical solution. This type of animal liability insurance exists precisely to fill the gap left by standard renters policies.

How Much Coverage Do You Actually Need?

When you are shopping for renters insurance with pet liability coverage, the most important number is your liability limit. Most standard renters policies offer somewhere between $100,000 and $300,000 in personal liability coverage. That sounds like a lot until you look at the cost table above.

For a single dog with no bite history and a lower-risk breed, $100,000 might be adequate. For anyone else — larger dogs, restricted breeds, households with multiple pets, or anyone living in a densely populated area — pushing toward $300,000 is smarter. And if you have real assets to protect, an umbrella policy on top of your renters coverage gives you $1 million or more in additional liability protection for a surprisingly low monthly premium.

| Liability Limit | Est. Monthly Add-On | Who It Makes Sense For |

| $100,000 | $10 – $16/month | Low-risk breed, no bite history, limited assets |

| $200,000 | $14 – $22/month | Medium-risk situation, multiple dogs |

| $300,000 | $18 – $28/month | Larger dogs, urban environment, higher assets |

| $1M+ umbrella | $15 – $30/month extra | Restricted breeds, high net worth, maximum peace of mind |

The National Association of Insurance Commissioners consistently advises consumers to choose liability limits based on their actual financial exposure — not on what is cheapest. For dog owners, that advice carries extra weight.

Also pay attention to the medical payments to others sub-limit. This is a no-fault coverage that pays small medical bills without requiring anyone to sue you. It typically runs $1,000 to $5,000 and can resolve minor incidents before they escalate. Good renters insurance that covers pets will include this.

How Much Does Dog Liability Insurance Cost?

The first thing most people want to know is how much does dog liability insurance cost. The answer genuinely depends on several variables — but for the majority of dog owners with standard breeds and no bite history, it is much less than you probably expect.

Adding renters insurance with dog coverage to an existing policy typically costs an extra $5 to $15 per month. That is less than a streaming subscription. For that amount, you get potentially hundreds of thousands of dollars in protection.

When the situation is more complicated — restricted breed, prior bite history, higher-risk location — standalone pet liability insurance for dogs through a specialty insurer typically runs $30 to $100 per month. Still reasonable when you consider the alternative.

What Moves the Price Up or Down

- Breed: The single biggest factor. Restricted breeds mean higher premiums or specialty policies

- Bite history: A dog with a prior bite is a much harder risk to place — expect significantly higher premiums

- Your liability limit: Higher limits cost more, but the incremental difference is usually small

- Where you live: States with strict liability laws and dense urban populations tend to have higher rates

- Your insurer: Rates vary more than people realize — always compare multiple quotes

Just as finding specialized coverage for unique needs sometimes requires looking beyond the obvious options, the same applies to dog liability insurance cost comparisons. The right fit depends on your specific situation.

Finding the Best Insurance for Renters with Pets

Not all renters policies treat pet owners the same way. Finding the best renters insurance for pet owners means looking at more than just the monthly premium. Here is what actually matters.

Breed Policy — Ask First, Compare Second

Before anything else, find out whether your insurer restricts your breed. This should be your first question — not an afterthought. Policies that offer renters insurance that covers dogs without breed restrictions are genuinely valuable, even if they cost slightly more.

Liability Limits and Flexibility

Look for policies where you can select $300,000 in personal liability, not just $100,000. The flexibility to increase limits matters, especially as your financial situation changes over time.

Off-Premises Coverage

Does the renters insurance dog bite protection follow your dog when you leave home? If your dog bites someone at the park or during a walk, does coverage apply? Some policies say yes, some say no. This is worth confirming.

Insurer Financial Strength

A policy is worthless if the company cannot pay the claim. Check insurer ratings through AM Best and review customer satisfaction scores from J.D. Power. Cheap premiums from a financially shaky insurer are not a deal.

Bundling and Discounts

Some insurers offer meaningful bundling discounts. Companies like Erie Insurance are known for strong liability coverage and competitive pricing for renters. If you are budget-conscious, exploring affordable insurance options is also worth your time — you might find better terms than you expect.

Standalone Pet Liability Insurance vs. Adding a Rider

When your standard renters policy does not offer sufficient renters insurance with dog bite coverage, you have two directions to go.

Standalone Dog Liability Insurance

Standalone pet liability insurance for dogs is sold as its own separate policy. It is designed specifically for situations where standard renters insurance falls short — usually because of breed restrictions or prior bite history. These policies typically cover:

- Bite injuries to third parties

- Property damage your dog causes to others

- Legal defense and settlement costs

- Off-premises incidents at parks, walking trails, or other locations

This type of dog owner liability insurance is underwritten by specialty carriers who are comfortable with risks that mainstream companies avoid. Premiums are higher, but for owners of restricted breeds or dogs with bite history, this is often the only realistic path to canine liability insurance.

Adding a Rider to Your Existing Policy

If your insurer restricts your breed but is willing to negotiate, ask about adding a canine liability coverage endorsement. Not every company offers this, but some will agree — particularly if your dog has completed a certified obedience training program and has no documented bite incidents.

The Consumer Financial Protection Bureau has useful resources on understanding the difference between base policy coverage and add-on endorsements — helpful reading before you get on the phone with your insurer.

What If Your Dog Has Already Bitten Someone?

This is one of the trickier situations in the renters insurance for dogs world. If your dog has a documented bite history, will renters insurance cover dogs with that kind of record? Honestly, probably not through a standard insurer — at least not without complications.

Most mainstream insurance companies will do one of three things when they find out your dog has bitten before:

- Exclude that specific dog from coverage while insuring everything else

- Decline to write the policy at all

- Offer coverage with a much higher premium and a lower sub-limit for dog-related incidents

If you are in this situation, your best option is animal liability insurance through a specialty underwriter. These companies exist specifically to cover risks that standard carriers will not touch. Coverage is usually available if the dog has undergone behavioral rehabilitation and can demonstrate a clean record since the incident.

One genuinely useful move: get your dog AKC Canine Good Citizen certified. Several specialty insurers view this favorably when underwriting dog liability insurance for renters for dogs with prior incidents. It will not erase the history, but it signals that the risk has been actively managed — and that can reduce your dog liability insurance cost meaningfully.

Dog Damage to Your Rental Unit — Who Pays?

This is probably the most misunderstood area of pet renters insurance. People assume that because they have insurance, pet damage to the apartment is covered. It almost never is.

Does renters insurance cover pet damage to the rental unit? No. Does it cover renters insurance pet damage to your own furniture? Also no. Your renters policy is liability coverage — it protects you when your dog hurts other people or their property, not when your dog destroys things in your home.

Here is how rental pet damage typically plays out:

- Normal wear and tear: The landlord’s responsibility — a bit of wear on carpets over a year is expected

- Actual pet damage: Scratched floors, chewed trim, stained carpet — this comes out of your security deposit

- Damage beyond the deposit: Your landlord can pursue you in small claims court for the remainder — renters insurance will not cover this

The most practical protection against tenant insurance pet damage disputes is a thorough move-in inspection, documented with photos, combined with a security deposit that reflects the reality of having a large dog. Some landlords also charge a separate pet deposit — worth agreeing to if it means being allowed to keep your dog.

For a broader understanding of how Ohio renters policies handle these kinds of landlord-tenant situations, read our guide on Ohio renters insurance policies.

A Practical Guide to Getting the Right Coverage

Shopping for renters insurance with dog bite coverage is not complicated once you know what to look for. Here is a straightforward process to get it right.

- Know your dog’s risk profile. Breed, size, temperament, bite history — have this information ready before you contact any insurer.

- Always disclose your dog. Never omit your pet from an insurance application. If your dog bites someone and the insurer finds out you hid it, they can deny the claim entirely.

- Get at least three quotes. Rates for pet renters insurance vary significantly. What one company charges $30 for, another might charge $15.

- Ask specific questions. Does coverage apply off-premises? Is my breed restricted? What is the sub-limit for dog bite claims specifically?

- Consider an umbrella policy. For $15 to $30 extra per month, you can add $1 million or more in additional liability coverage. For dog owners with real assets, this is worth serious consideration.

- Review annually. Your dog ages, your assets grow, your risk profile changes. Review your renters insurance with pet coverage every policy renewal to make sure your limits still make sense.

Ohio Dog Owners: What You Specifically Need to Know

Ohio operates under one of the stricter dog bite liability frameworks in the country. Under Ohio Revised Code Section 955.28, dog owners are strictly liable for injuries caused by their dogs — meaning you do not have to know your dog was dangerous for liability to attach. One incident, and you are on the hook.

This makes renters insurance with dog bite coverage not just smart but practically essential for Ohio renters who own dogs. The strict liability standard removes the wiggle room that exists in states with one-bite rules.

Our comprehensive guide on renters insurance options for Ohio residents covers the full state-specific legal framework, including how Ohio’s strict liability law interacts with your insurance coverage and what limits make sense given local claim trends.

A few other states worth knowing about if you are planning a move:

- California — strict liability, no one-bite rule, owner responsible for all bites in public or lawfully-accessed private space

- Texas — modified one-bite rule, prior knowledge of aggression required in most cases

- Florida — strict liability with comparative negligence factored in

- New York — primarily one-bite rule, with some strict liability exceptions

Frequently Asked Questions

Closing Thoughts: Do Not Wait Until Something Goes Wrong

Dog ownership is one of the genuinely great things in life. But it comes with financial responsibilities that a lot of renters simply are not prepared for. One bite incident — even a minor one — can result in a lawsuit that costs more than most people earn in a year.

The case for renters insurance with dog bite coverage is not complicated. It protects you from liability that is real, that is common, and that can be financially devastating without the right coverage in place.

What does renters insurance cover pets for? Liability — the financial exposure you face when your dog injures someone else. What it does not cover is renters insurance pet damage to your own belongings, or damage your dog causes to the rental unit. Knowing that distinction helps you plan properly.

If you are in Ohio or planning to move there, start with our guide on renters insurance in Ohio to understand the state-specific rules that affect your coverage decisions. Then come back and apply what you have learned here to make sure your dog — whatever the breed, whatever the history — is properly accounted for in your policy.

The right best renters insurance for pet owners policy exists for your situation. You just need to look for it with the right information in hand — and now you have it.